By James G. Burns, Esq.

Law Office of James Burns — Estate Planning & Asset Protection, Aliso Viejo, California

Imagine this...

A client's portfolio rockets up 60% inside a Grantor Retained Annuity Trust (GRAT). They've just created millions in value—yet unless they lock in that growth before the GRAT ends, much of that upside could vanish in a market pullback or miss the transfer to heirs.

Now imagine being able to capture that gain strategically, transfer it to heirs tax-free, and then recycle the original asset into another GRAT for compounding value. All without burning a penny of their lifetime gift exemption.

We're entering a new era of precision-driven estate planning. The strategy of automated GRAT swaps, when paired with long-term tax-deferral vehicles like Private Placement Life Insurance (PPLI), is fast becoming one of the most elegant and effective legacy techniques available to sophisticated families.

Many clients—and some advisors—view GRATs as overly complicated, outdated, or only suitable for ultra-high-net-worth individuals. In truth, GRATs are among the most accessible and scalable estate planning tools available.

Misconceptions include:

- "GRATs are only for billionaires."

- "GRATs don't work unless interest rates are high."

- "The IRS is cracking down on GRATs."

In reality, GRATs remain fully supported by the Tax Code, including landmark case law like Walton v. Commissioner. And with the right asset and execution strategy, they can unlock vast value for founders, executives, and real estate families alike.

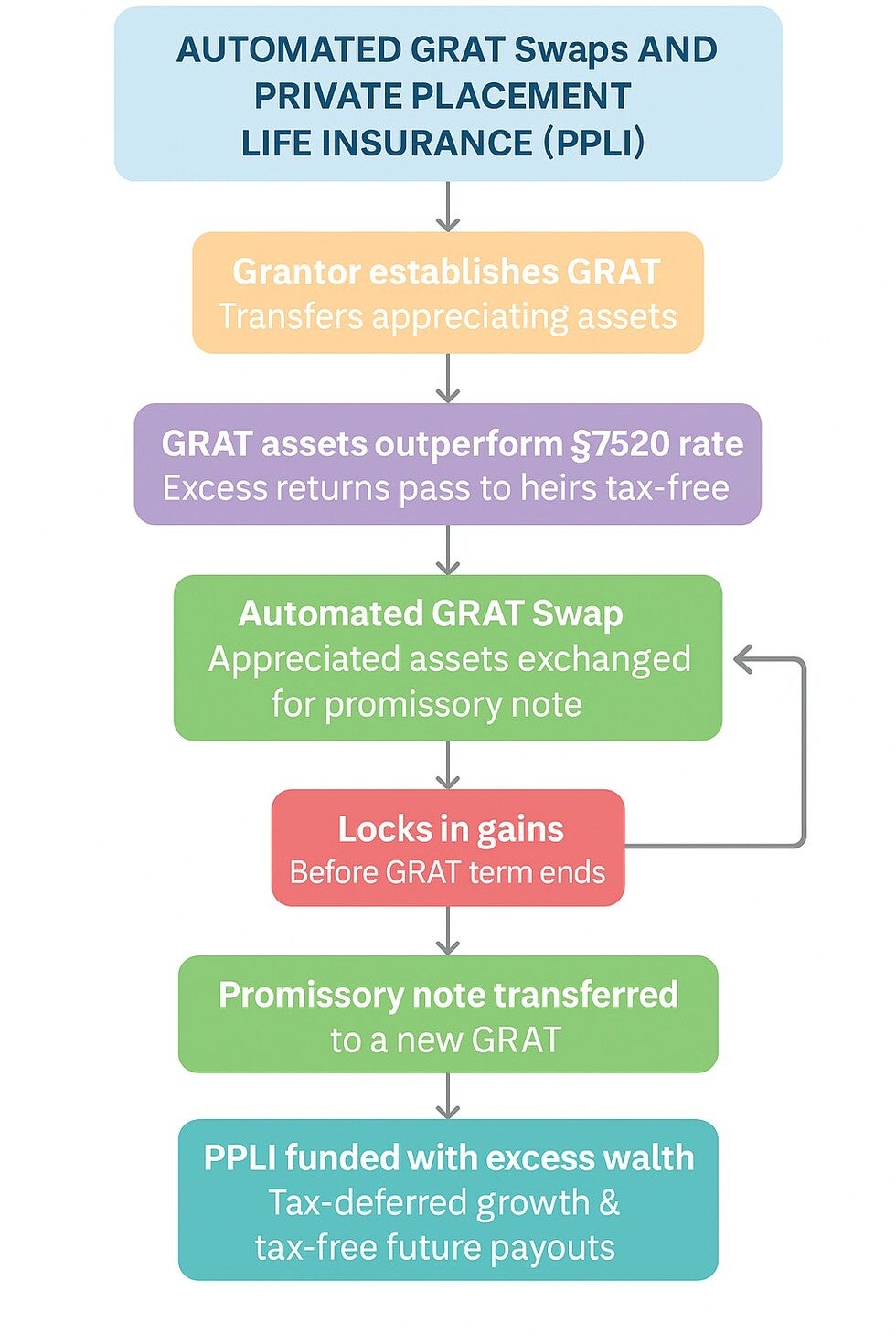

A Grantor Retained Annuity Trust (GRAT) is a powerful estate planning tool under IRC §2704. It allows a grantor to transfer the future appreciation of an asset to their beneficiaries without paying gift tax, as long as the asset growth exceeds the Section 7520 rate (a hurdle rate published monthly by the IRS).

Here's how it works:

- The grantor contributes assets (typically appreciating stocks, LLC interests, or restricted shares) into the GRAT.

- The GRAT pays the grantor an annuity for a fixed term (e.g., 2–5 years).

- Any growth above the IRS's assumed rate (currently in the ~4% range) passes tax-free to the beneficiaries.

If the assets grow faster than the 7520 rate, the excess appreciation is transferred to heirs without triggering gift tax. This is especially valuable in volatile markets—or in years like 2020, 2024, and beyond when technology and private equity assets experience rapid valuation climbs.

One GRAT is powerful. But stacking GRATs—establishing new GRATs annually or even quarterly—can create a compounding conveyor belt of wealth transfer. Each new GRAT receives newly recycled assets or repurchased shares. Over time, the structure transfers a growing portion of wealth out of the estate. If one GRAT underperforms, others may still succeed. This staggered approach creates diversification by timing and allows advisors to rebalance strategies across market cycles.

A GRAT swap is a tactical strategy where the grantor swaps assets of equal value with the GRAT to lock in gains before a market downturn. For example:

- Asset in GRAT appreciates 60%

- Grantor substitutes the asset with a promissory note or cash equivalent of equal value

- The GRAT now holds a stable-value asset, and the appreciated asset is pulled back into the grantor's estate to be re-used in further planning

This strategy is fully compliant with IRS guidance under IRC §675(4)(C) and Rev. Rul. 2008-22, which confirm that substitution powers within a grantor trust do not trigger income or gift taxes.

Once a GRAT swap is executed and the appreciated asset is pulled into the grantor's estate, the next step is critical: redeploying that gain inside a Private Placement Life Insurance (PPLI) policy. Why PPLI?

- Provides tax-free investment growth under IRC §§72 and 7702

- Allows customization of subaccount portfolios

- Offers death benefit leverage and asset protection

This combination allows families to convert tax-free GRAT gains into permanently tax-exempt wealth.

Despite their effectiveness, most GRAT swaps are mistimed—or missed altogether. Markets move quickly. Clients and advisors must manually monitor performance. It's difficult to catch the “peak” of appreciation in real time. What high-net-worth families need is a disciplined swap protocol — tied not to instinct, but to data and decision rules. When implemented, these protocols can be coupled with PPLI integration, creating multi-layered planning where appreciation is captured and then shielded from future taxation.

Here's a real-world case study: Amanda, a 45-year-old tech founder in California, contributes $15M of pre-IPO shares to a 3-year GRAT. Within 20 months, the shares appreciate to $25M. Amanda executes a swap for a $25M promissory note. The appreciated shares are transferred into a South Dakota dynasty trust that owns a PPLI policy on Amanda's life. The PPLI subaccount is customized to mirror her risk preferences. Amanda locks in $10M of tax-free GRAT value to her heirs. The growth continues inside the PPLI policy free from income tax, and Amanda retains liquidity and asset protection within the SD trust.

FAQs:

- Can I integrate a GRAT strategy with my existing estate plan or living trust? Yes. GRATs are typically standalone irrevocable trusts, but they complement living trusts or dynasty plans.

- Is this strategy only for tech entrepreneurs or high-net-worth families? While most powerful for appreciating assets, clients with $5M–$10M estates can benefit.

- Can this strategy work with real estate or rental property? Yes, with added complexity: appraisals, liquidity planning, and income handling.

- How does this compare to 1031 exchanges? GRATs optimize estate tax reduction. 1031s defer income tax. Both can be layered.

- What happens if the IRS audits this structure? These strategies are IRS-acknowledged. Ensure proper documentation and valuations.

Legal Basis:

- IRC §2704, §7520, §675(4)(C), Rev. Rul. 2008-22

- Walton v. Commissioner, 115 T.C. 589 (2000)

- For PPLI: IRC §72, §7702, Rev. Rul. 2003-91

Related Reading: For deeper estate planning insights, see our articles on Living Trusts in California, ILITs, and California Estate Planning FAQs.

Let's Help You Transfer More, Tax-Free

At the Law Office of James Burns, we specialize in designing advanced wealth transfer strategies that integrate GRATs, Private Placement Life Insurance, and cutting-edge trust planning. If you want to:

- Optimize your GRAT before the window closes

- Use swaps and structured notes to lock in gains

- Create a dynasty trust structure with built-in tax shielding

Schedule a confidential strategy session today.

📞 (949) 305-8642

🌐 www.jamesburnslaw.com

📍 Based in Aliso Viejo, Serving Orange County and California Families Statewide

DISCLAIMER: This blog post is for informational purposes only and does not constitute legal, tax, or investment advice. Please consult qualified advisors before implementing any strategy. Results may vary depending on personal circumstances and market conditions.

© 2025 Law Office of James Burns. All rights reserved.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment