Introduction: Understanding PPLI and Its Importance for High-Net-Worth Individuals

In today's complex financial landscape, high-net-worth individuals face unique challenges in preserving and growing their wealth efficiently. One powerful tool that has emerged as a game-changer is Private Placement Life Insurance (PPLI). This innovative insurance product offers unparalleled tax advantages, investment flexibility, and personalized financial planning opportunities designed specifically for affluent investors.

In this article, you will learn what PPLI entails, how it optimizes your wealth management strategy, and why it is becoming essential for those seeking to safeguard their financial legacies while maximizing growth potential.

Why PPLI Matters for Wealth Preservation

For individuals with significant assets, traditional wealth management vehicles may not address all needs, especially regarding taxation and asset protection. PPLI can fill these gaps by offering a tailored approach that aligns with sophisticated financial goals.

What You'll Gain from This Article

- An in-depth understanding of PPLI and its components

- Insight into the tax benefits exclusive to PPLI policies

- Practical steps to implement PPLI in your portfolio

- Real-life examples showcasing transformative results

What is PPLI? An Overview of Private Placement Life Insurance

Private Placement Life Insurance (PPLI) is a specially designed variable universal life insurance policy offered to high-net-worth individuals. Unlike traditional life insurance, PPLI combines the benefits of life protection with sophisticated investment options and tax efficiencies.

Defining PPLI

PPLI allows policyholders to invest in a customized portfolio of assets within a life insurance wrapper, providing death benefits alongside potential for tax-deferred growth.

- Tailored investment choices reflecting the individual's risk tolerance and financial objectives

- Flexible premium payments accommodating estate and liquidity planning

- Variable death benefits that can adjust based on policy performance

How PPLI Differs from Traditional Insurance

While traditional insurance products focus primarily on death benefits with limited investment options, PPLI integrates investment strategies for wealth accumulation.

Eligibility and Suitability

PPLI is typically available to accredited investors or those meeting high net worth thresholds, ensuring alignment with complex financial needs.

- Minimum investment requirements often start at $1 million or more

- Suitable for individuals seeking bespoke wealth management solutions

Regulatory Environment

PPLI policies comply with insurance and securities regulations, offering a secure and transparent framework for investors.

The Tax Advantages of PPLI: How It Optimizes Wealth Management

One of the most compelling reasons wealth managers recommend PPLI is its superior tax efficiency. It provides multiple avenues to legally minimize tax liabilities, enhance wealth transfer strategies, and increase overall returns.

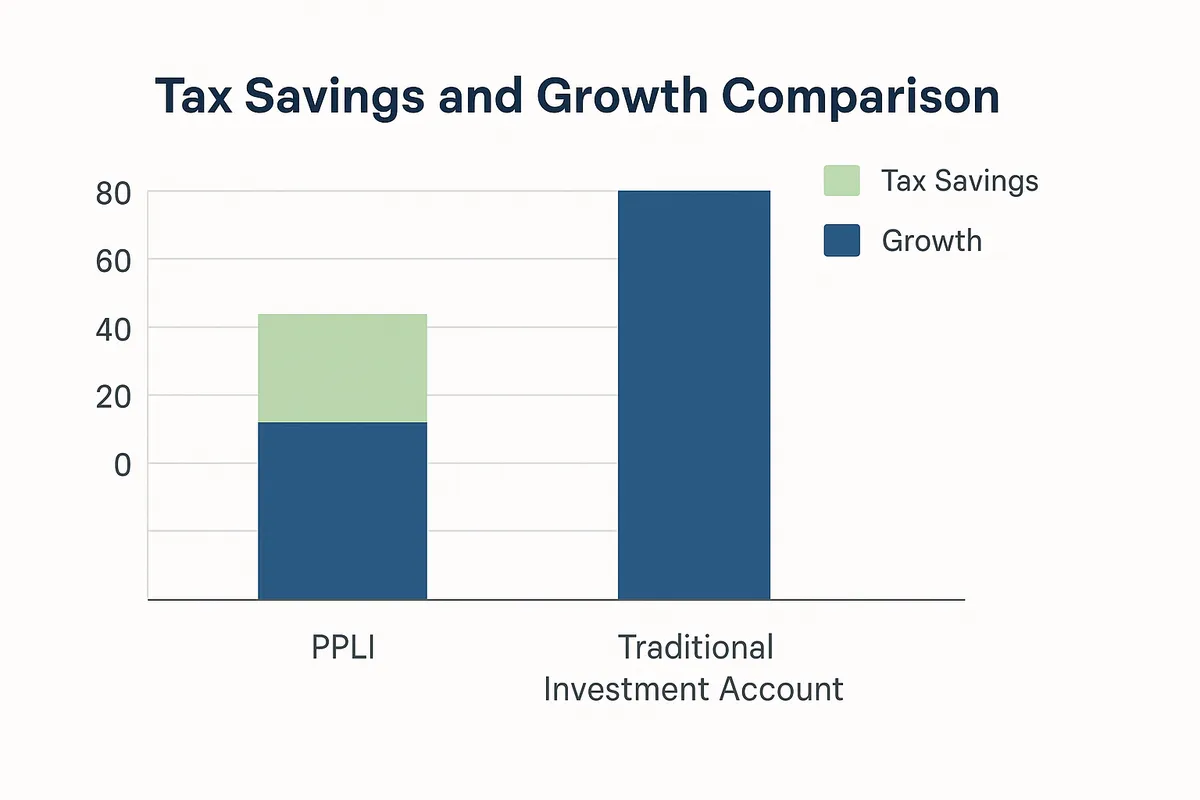

Tax-Deferred Growth

The investment gains inside a PPLI policy grow on a tax-deferred basis.

- Earnings and capital gains are not taxed annually, allowing compounding without drag

- Access to underlying investments without triggering immediate tax events

Tax-Free Death Benefit

The death benefit paid to beneficiaries is generally income tax-free, providing a powerful estate planning tool.

- Facilitates efficient wealth transfer without estate tax erosion

- Offers liquidity to heirs for estate settlement costs

Mitigation of Capital Gains Taxes

Since investments are held inside the policy, sales of assets do not trigger capital gains taxes.

- Enables strategic portfolio rebalancing without immediate tax consequences

- Enhances after-tax returns over time

International Tax Considerations

For globally mobile individuals, PPLI can be structured to optimize cross-border tax exposure and compliance.

- Offers privacy and asset protection in multiple jurisdictions

- May reduce withholding taxes on income distributions

Personalized Financial Planning Through PPLI

PPLI is not a one-size-fits-all product; it is highly customizable to fit individual financial goals and risk profiles.

Tailored Investment Portfolios

Policyholders can select from a broad range of asset classes within their PPLI.

- Equities, bonds, hedge funds, private equity, and alternative investments

- Ability to exclude unsuitable assets or sectors

Flexible Premium Structures

Premium payments can be adjusted over time to accommodate life events and liquidity needs.

- Lump-sum or periodic premium payments

- Potential to increase or reduce premiums based on financial circumstances

Estate and Succession Planning

PPLI facilitates smooth wealth transfer aligned with family governance strategies.

- Options for naming multiple beneficiaries or trusts

- Integration with trusts to control timing and amount of distributions

Access to Cash Values

Policyholders may access cash values through loans or withdrawals, offering liquidity without disrupting the investment portfolio.

- Loans are generally tax-free if managed properly

- Provides emergency funds or opportunities without triggering asset sales

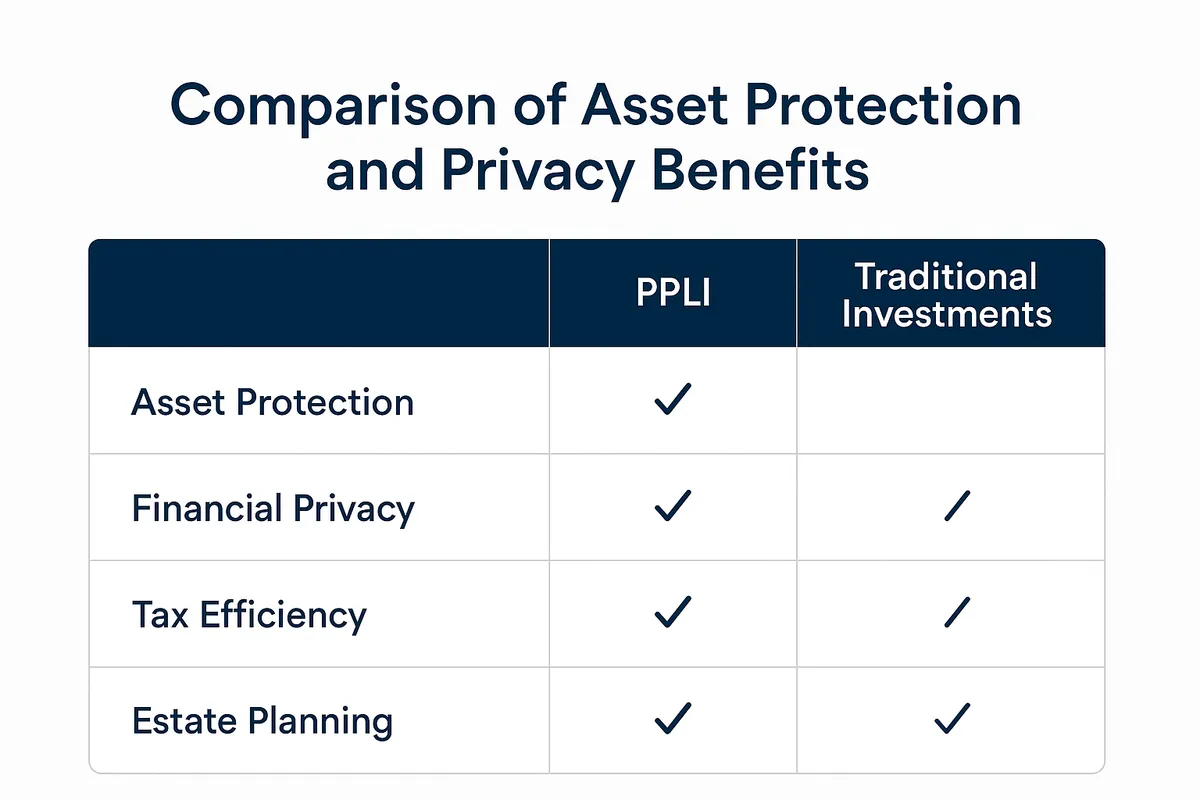

Asset Protection and Privacy Benefits of PPLI

Beyond tax efficiency, PPLI offers robust asset protection and confidentiality, critical for wealthy individuals.

Shielding Assets from Creditors

In many jurisdictions, the cash values and death benefits within a PPLI policy enjoy protection from creditors.

- Provides a legal barrier against lawsuits or claims

- Enhances financial security and peace of mind

Enhanced Privacy

Unlike publicly registered investment accounts, PPLI policies offer private ownership structures.

- Confidentiality of holdings and transactions

- Reduced public disclosure, safeguarding sensitive financial information

Protection from Market Volatility

The insurance wrapper separates the policy assets from the policyholder's personal estate, potentially shielding from certain market risks.

- Allows strategic investment while limiting exposure to personal liabilities

International Asset Protection

For individuals with assets across borders, PPLI can be structured in jurisdictions with favorable privacy laws.

- Supports multi-jurisdictional estate planning

- Mitigates risks associated with political and economic instability

Investment Flexibility with PPLI: A Tailored Approach

Investment flexibility is a cornerstone of PPLI, allowing policyholders to align their portfolios with personal preferences and market opportunities.

Broad Investment Universe

PPLI permits investments beyond traditional stocks and bonds.

- Access to hedge funds, private equity, real estate, and commodities

- Ability to incorporate alternative strategies that may not be available in standard insurance products

Control Over Asset Selection

Policyholders retain significant discretion over the underlying investments, subject to insurer approval.

- Enables alignment with risk appetite and ethical considerations

- Facilitates dynamic reallocation based on market conditions

Tax-Efficient Portfolio Management

Because the investments reside inside the PPLI, rebalancing and trading do not trigger immediate tax liabilities.

- Encourages active portfolio management without tax drag

- Supports long-term wealth growth strategies

Integration with Broader Investment Strategies

PPLI can complement other financial instruments and investment vehicles.

- Coordinates with trusts, family offices, and charitable giving plans

- Provides a cohesive approach to overall wealth management

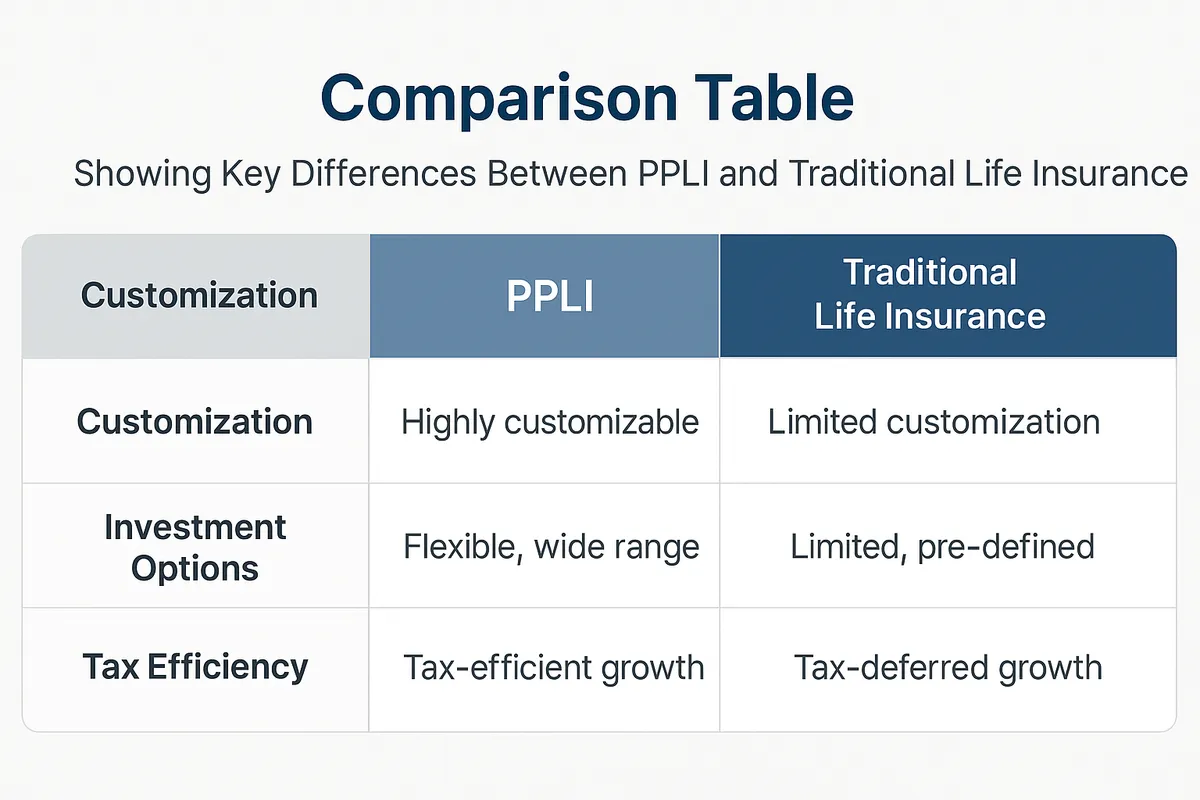

Comparing PPLI with Traditional Life Insurance Products

Understanding how PPLI stacks up against conventional life insurance products highlights its unique advantages for high-net-worth individuals.

Coverage and Death Benefit Structures

PPLI offers variable death benefits tied to underlying investment performance, unlike fixed benefits of traditional policies.

- Potential for increased death benefits in strong market conditions

- Flexibility to adjust coverage as financial situations evolve

Investment Opportunities

Traditional policies typically invest in limited, insurer-managed funds.

- PPLI provides broader, client-directed investment choices

- Greater potential for customized portfolio construction

Cost Considerations

While PPLI generally requires higher upfront minimums and fees, the tax efficiencies and investment control often justify the expense.

- Traditional life insurance may have lower premiums but limited upside

Suitability for Wealth Planning

PPLI is designed for sophisticated estate and tax planning needs, whereas traditional policies focus on basic life coverage.

- Ideal for clients with complex financial goals

- Not typically recommended for mass-market clients

How PPLI Fits into a Comprehensive Wealth Management Strategy

Integrating PPLI into your broader financial plan can unlock synergistic benefits for wealth preservation, growth, and transfer.

Complementing Other Investment Vehicles

PPLI works alongside brokerage accounts, trusts, and retirement plans to diversify risk and optimize tax outcomes.

- Enhances overall portfolio diversification

- Reduces tax drag on investment gains

Enhancing Estate Planning

The policy's death benefit and cash value features support efficient wealth transfer strategies.

- Provides liquidity for estate taxes

- Enables intergenerational wealth transfer in a controlled manner

Supporting Philanthropic Goals

PPLI can be structured to include charitable beneficiaries or foundations.

- Facilitates tax-efficient charitable giving

- Supports family legacy and values

Risk Management Integration

The insurance aspect of PPLI adds protection against premature death and market volatility.

- Stabilizes financial plans amid uncertainties

Case Studies: Real-Life Examples of PPLI Transforming Financial Futures

Examining real-world applications of PPLI illustrates its transformative potential for affluent individuals.

Case Study 1: Tax-Efficient Growth for a Family Office

A family office with $20 million in investable assets used PPLI to shield investment gains from annual taxation.

- Achieved tax-deferral leading to a 15% increase in net portfolio value over 5 years

- Enhanced estate planning with flexible beneficiary designations

Case Study 2: Asset Protection for a Business Owner

A successful entrepreneur deployed PPLI to protect wealth from potential creditor claims.

- Secured $10 million in assets within the policy

- Benefited from confidentiality and legal asset protection

Case Study 3: International Wealth Planning for a Global Citizen

A dual-resident investor structured PPLI across jurisdictions to optimize tax efficiency and privacy.

- Reduced cross-border tax exposure

- Simplified estate administration for heirs

Lessons Learned

- Tailoring PPLI to individual needs maximizes benefits

- Professional guidance is essential for complex structuring

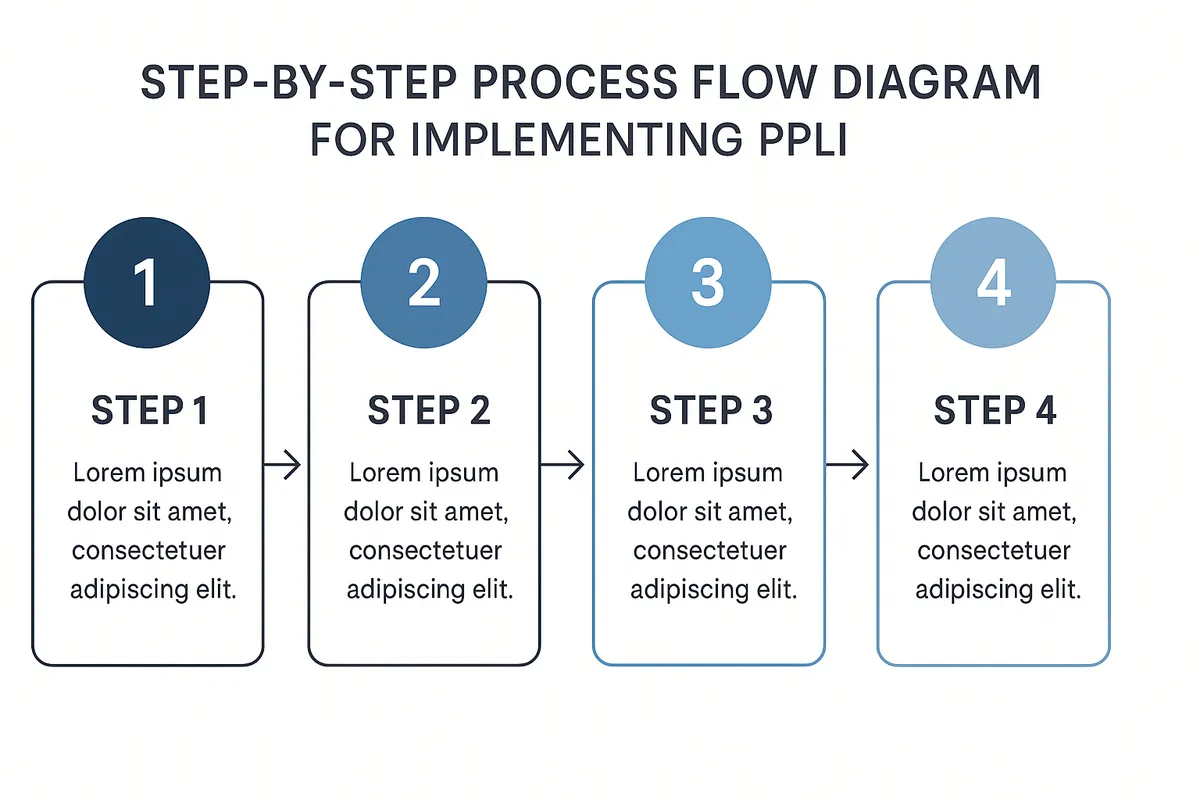

Steps to Implement PPLI in Your Financial Plan

Adopting PPLI involves a structured process to ensure alignment with your unique goals and compliance requirements.

Step 1: Assess Eligibility and Objectives

Evaluate your financial status, investment goals, and tax considerations to determine if PPLI fits your needs.

- Work with a qualified financial advisor

- Clarify estate planning priorities

Step 2: Choose a Reputable Insurer and Policy Structure

Select an insurer experienced in PPLI and design a policy that reflects your investment preferences and risk tolerance.

- Review insurer ratings and compliance records

- Customize investment options within the policy

Step 3: Fund the Policy and Establish Governance

Transfer assets or premiums into the policy while setting up beneficiary designations and trust arrangements if applicable.

- Coordinate with legal counsel for estate documents

- Implement ongoing management protocols

Step 4: Monitor and Adjust

Regularly review policy performance and adjust investments or premiums to adapt to changing circumstances.

- Schedule annual policy reviews

- Rebalance portfolio as needed

Step 5: Estate and Succession Integration

Ensure PPLI complements your broader estate and succession plans.

- Align with trusts and wills

- Communicate plans with heirs and advisors

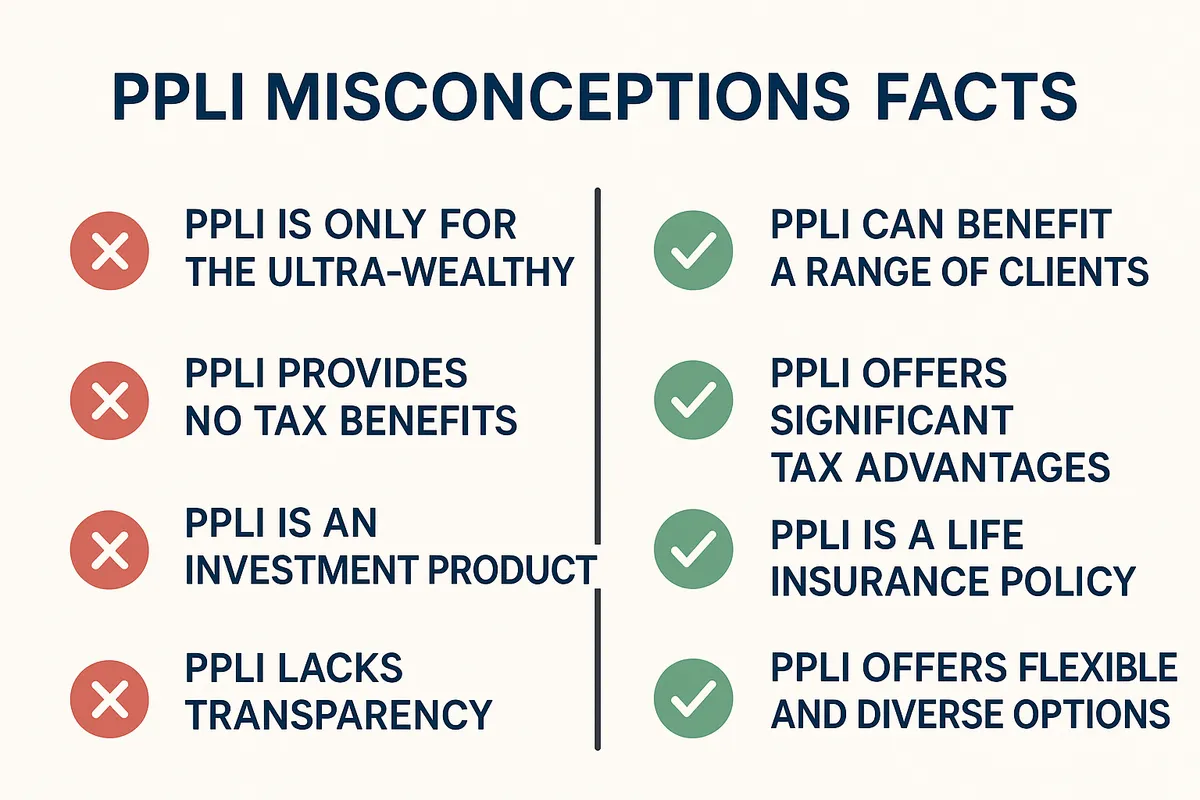

Common Misconceptions About PPLI and How to Overcome Them

Despite its advantages, PPLI is often misunderstood, leading to hesitation or missed opportunities.

Myth 1: PPLI is Only for Ultra-High-Net-Worth Individuals

While mostly suited for wealthy clients, minimums vary, and tailored solutions exist for diverse profiles.

- Some insurers offer lower entry points

- Customized structures can accommodate smaller portfolios

Myth 2: PPLI is Too Complex and Costly

Though sophisticated, the benefits often outweigh costs when properly structured.

- Professional guidance simplifies complexity

- Long-term tax savings justify upfront expenses

Myth 3: Investments Within PPLI Are Limited

Contrary to belief, PPLI offers broad investment flexibility.

- Access to alternative assets unavailable in typical insurance products

Myth 4: PPLI Does Not Provide Real Asset Protection

In many jurisdictions, PPLI offers strong legal protection against creditors.

- Must be properly structured and compliant

Myth 5: PPLI Is Just Another Life Insurance Product

PPLI is a hybrid solution uniquely combining life insurance with investment and tax planning.

- Offers advantages far beyond traditional policies

Conclusion: Transform Your Financial Future with PPLI Today

Private Placement Life Insurance (PPLI) represents a paradigm shift in wealth management for high-net-worth individuals. By combining tax efficiency, investment flexibility, asset protection, and personalized planning, it empowers you to optimize your financial future with confidence.

If you are seeking sophisticated solutions to grow, protect, and transfer your wealth effectively, now is the time to explore how PPLI can be tailored to your unique goals. Partner with experienced advisors to design a strategy that transforms your financial legacy today.

Take the first step toward a more secure and prosperous tomorrow by considering PPLI as a cornerstone of your wealth management plan.

FAQ

Q1: What does PPLI stand for?

PPLI stands for Private Placement Life Insurance, a customizable life insurance product for high-net-worth individuals.

Q2: Who is eligible for PPLI?

Typically, accredited investors or individuals with investable assets of $1 million or more qualify.

Q3: How does PPLI differ from traditional life insurance?

PPLI offers variable investment options, tax advantages, and flexible premium structures unlike traditional fixed policies.

Q4: What are the tax benefits of PPLI?

Tax-deferred growth of investments, tax-free death benefits, and avoidance of capital gains taxes on asset sales within the policy.

Q5: Can I invest in alternative assets through PPLI?

Yes, PPLI policies allow investments in hedge funds, private equity, real estate, and other alternatives.

Q6: Is PPLI suitable for estate planning?

Absolutely. It provides liquidity for estate taxes and facilitates efficient wealth transfer.

Q7: Are the assets in a PPLI policy protected from creditors?

In many jurisdictions, assets held in PPLI enjoy legal protection from creditors.

Q8: How much does PPLI cost?

Costs vary by policy but usually include premiums, insurance charges, and administrative fees.

Q9: Can I access cash values in a PPLI policy?

Yes, through policy loans or withdrawals, often on a tax-efficient basis.

Q10: Does PPLI require annual tax filings?

Investment growth within the policy is tax-deferred, generally reducing tax reporting requirements.

Q11: Can PPLI be used for charitable giving?

Yes, it can be structured to benefit charities as part of philanthropic planning.

Q12: Is PPLI available internationally?

Yes, many insurers offer PPLI in multiple jurisdictions, accommodating global clients.

Q13: How flexible are premium payments?

Premiums can be flexible, with options for lump-sum or scheduled payments.

Q14: What investment control do policyholders have?

Policyholders can select and change investments within approved options.

Q15: Are PPLI policies regulated?

Yes, they comply with insurance and securities regulations.

Q16: Can PPLI help reduce estate taxes?

By removing assets from the taxable estate, PPLI can reduce estate tax exposure.

Q17: How does PPLI protect privacy?

Ownership and investment details are typically confidential and not publicly disclosed.

Q18: What happens if the policyholder dies prematurely?

Beneficiaries receive a death benefit, often income tax-free.

Q19: Can I switch insurers if unsatisfied?

Policyholders may surrender or transfer policies subject to terms and potential fees.

Q20: How do I start the process of obtaining PPLI?

Consult a qualified financial advisor to assess suitability and initiate policy design and underwriting.

Q21: Does the policy performance affect the death benefit?

Yes, variable death benefits depend on the underlying investment performance.

Q22: Can PPLI be combined with trusts?

Yes, integrating PPLI with trusts enhances estate and succession planning.

Q23: Is PPLI suitable for younger investors?

Generally designed for established high-net-worth individuals but may be considered depending on circumstances.

Q24: Does PPLI pay dividends?

Dividends depend on investment performance within the policy.

Q25: Are there risks associated with PPLI?

Investment risks apply as with any portfolio; proper management and advice mitigate these risks.

Q26: Can PPLI help with business succession planning?

Yes, it can provide liquidity and facilitate smooth transfer of business interests.

Q27: How often can I change my investment selections?

Frequency varies by policy but many allow periodic adjustments.

Q28: What role does insurance underwriting play?

Underwriting assesses insurability and influences premium costs.

Q29: Can I name multiple beneficiaries?

Yes, policies allow multiple beneficiaries and contingent designations.

Q30: Does PPLI require medical exams?

Absolutely, at these ranges a carrier is going to require full medical underwriting.

Take the Next Step

If you're considering Private Placement Life Insurance (PPLI) or want to know how it integrates into your estate and asset protection planning, now is the time to get clear answers. The Law Office of James Burns specializes in advanced wealth protection strategies for high-net-worth individuals, families, and business owners. Schedule a confidential consultation today and take the first step toward building your FortressWall™ of protection.

📞 (949) 305-8642

🌐 www.jamesburnslaw.com

Disclaimer

The information provided in this blog is for educational purposes only and does not constitute legal, tax, or financial advice. Laws and regulations are subject to change, and the application of such laws depends on the specific circumstances of each individual. You should consult with a qualified attorney, tax professional, or financial advisor before making any decisions regarding estate planning, asset protection, or investment strategies.

Intellectual Property Notice

© 2025 Law Office of James Burns. All rights reserved. FortressWall™ and Legacy Trust™ are proprietary frameworks of the Law Office of James Burns. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the copyright owner, except in the case of brief quotations for non-commercial use with proper attribution.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment