Introduction: Understanding the Importance of a Living Trust

As a young professional, building your financial foundation is both exciting and challenging. You're focused on growing your assets, planning for career advancement, and envisioning a secure future. But have you considered how to protect what you've worked so hard to accumulate? Setting up a living trust is a powerful step toward safeguarding your wealth and ensuring your wishes are honored if life takes an unexpected turn.

In this article, you'll learn what a living trust is, the top five benefits of establishing one, and practical steps to set it up. By the end, you'll understand how this estate planning tool can offer peace of mind, control, and protection tailored to your unique needs.

What is a Living Trust? A Comprehensive Overview

Understanding the basics of a living trust is essential before diving into its benefits.

Definition and Purpose of a Living Trust

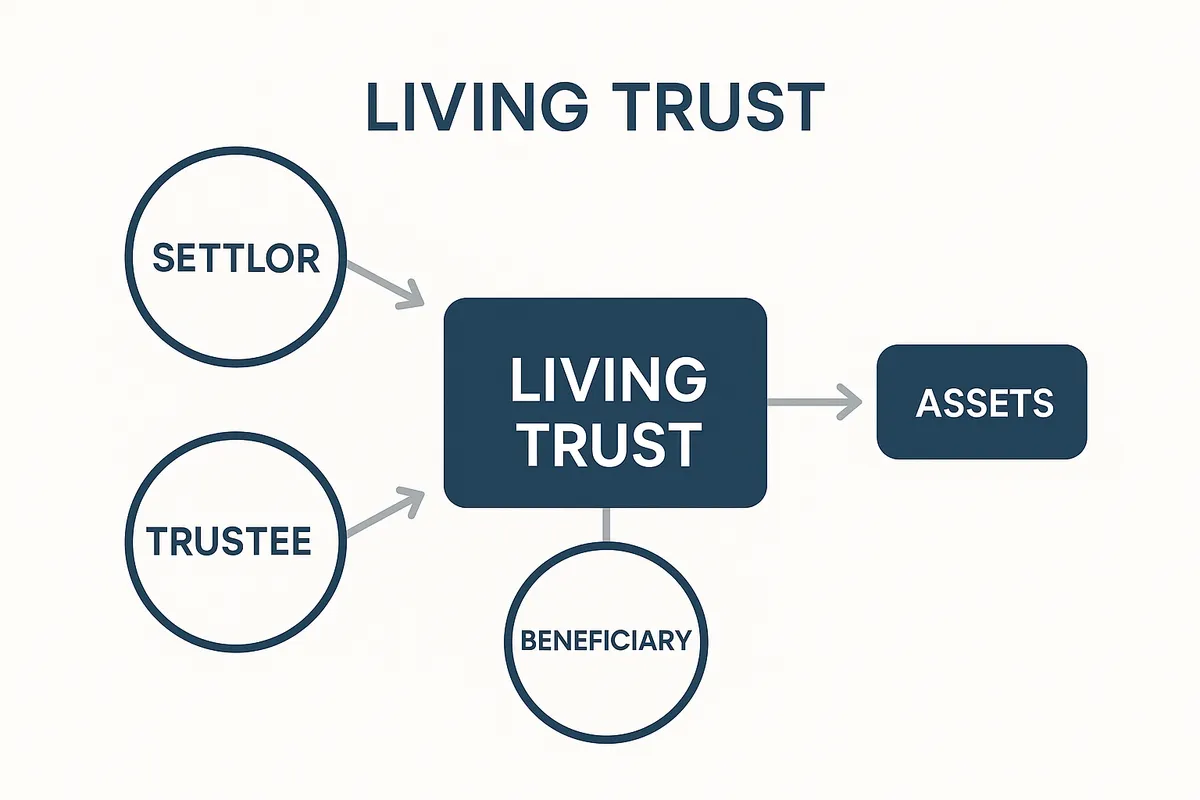

A living trust is a legal document that holds your assets during your lifetime and specifies how they should be managed and distributed after your death.

- It allows you to retain control over your assets while you're alive.

- It outlines directives for asset distribution without going through probate.

- It can be revocable or irrevocable, with revocable trusts being more common for personal estate planning.

Types of Living Trusts

Knowing the different types helps you choose the right one for your situation.

- Revocable Living Trust: Can be altered or revoked during your lifetime.

- Irrevocable Living Trust: Cannot be changed once established, often used for tax and asset protection.

- Testamentary Trust: Created as part of a will, activated after death.

How a Living Trust Works

It involves transferring assets into the trust, with a trustee managing them according to your instructions.

- You are typically the initial trustee.

- Upon death or incapacity, a successor trustee takes over.

- Assets held in trust bypass probate, speeding up distribution.

Benefit 1: Avoiding Probate and Ensuring Privacy

One of the biggest advantages of a living trust is the ability to avoid the probate process, which can be lengthy and public.

What is Probate?

Probate is the court-supervised process of validating a will and distributing assets.

- It can take months or even years.

- It incurs fees and legal expenses.

- Probate records are public, exposing your estate details.

How a Living Trust Bypasses Probate

Assets held in the trust pass directly to beneficiaries without court intervention.

- Saves time during estate settlement.

- Reduces legal and administrative costs.

- Maintains privacy by keeping asset details confidential.

Privacy Benefits for Young Professionals

Young professionals often want to keep their financial affairs private.

- Avoids exposing your growing assets to public scrutiny.

- Protects sensitive information from identity theft risks.

- Ensures your family's financial matters remain confidential.

Benefit 2: Flexibility and Control Over Your Assets

A living trust offers unparalleled flexibility and control, which is ideal for young professionals managing dynamic financial situations.

Retaining Control During Your Lifetime

You remain in charge of your assets and can modify the trust as your circumstances change.

- Add or remove assets as needed.

- Change beneficiaries or terms.

- Manage investments directly.

Managing Assets After Incapacity

The trust includes provisions for a successor trustee to manage your assets if you become incapacitated.

- Avoids court-appointed guardianship.

- Ensures continuous management of your finances.

- Protects your interests without interruption.

Customizing Distribution Terms

You can specify how and when beneficiaries receive assets.

- Set age thresholds for inheritance.

- Include conditions like educational milestones.

- Protect assets from creditors or divorce.

Benefit 3: Protecting Your Family and Beneficiaries

Your growing family and loved ones depend on you. A living trust helps provide for them securely.

Ensuring Smooth Transfer of Assets

The trust guarantees your assets go to the right people without delays.

- Prevents disputes among heirs.

- Avoids complications with intestacy laws.

- Provides clear instructions for distribution.

Protecting Minor Children

You can appoint guardians and set terms for managing assets on behalf of minors.

- Trust holds assets until children reach maturity.

- Successor trustee manages funds responsibly.

- Safeguards inheritance from misuse.

Shielding Beneficiaries from Creditors

Certain trusts offer protection from creditors or legal claims against beneficiaries.

- Limits risk of losing assets due to lawsuits.

- Provides financial security for vulnerable family members.

- Maintains long-term support for beneficiaries.

Supporting Special Needs Family Members

Special needs trusts can be incorporated to ensure beneficiaries receive care without affecting government benefits.

- Allows for supplemental support.

- Avoids disqualification from assistance programs.

- Provides peace of mind for caregivers.

Benefit 4: Planning for Incapacity and Unforeseen Events

Life can change unexpectedly. A living trust prepares you for the unknown.

What Happens If You Become Incapacitated?

Without proper planning, managing your assets can become complicated.

- Court may appoint a guardian or conservator.

- Family disputes may arise over control.

- Financial affairs could be neglected.

Role of the Successor Trustee

The trust designates someone to take over management if you're unable.

- Ensures seamless financial oversight.

- Follows your instructions precisely.

- Reduces stress on family during crises.

Incorporating Healthcare Directives

While a living trust primarily deals with assets, it can complement healthcare powers of attorney.

- Coordinate financial and medical decision-making.

- Provide comprehensive incapacity planning.

- Protect your autonomy and wishes.

Real-World Example: Young Professional with Growing Assets

Consider Sarah, a 32-year-old entrepreneur who set up a living trust after a minor car accident made her realize the importance of incapacity planning.

- Named her sister as successor trustee.

- Avoided potential guardianship battles.

- Maintained control over her business assets.

Benefit 5: Saving Time and Reducing Costs in Estate Management

Managing your estate efficiently preserves wealth for your beneficiaries.

Costs Associated with Probate

Probate involves fees that can erode your estate's value.

- Court filing fees.

- Attorney and executor fees.

- Appraisal and administrative expenses.

How a Living Trust Minimizes Expenses

By avoiding probate, a living trust reduces or eliminates many costs.

- Streamlines asset transfer.

- Lowers legal fees.

- Simplifies administration.

Time Savings for Your Loved Ones

Quick distribution helps beneficiaries access funds when needed.

- Reduces delays in inheritance.

- Eases emotional burden during bereavement.

- Allows faster resolution of financial affairs.

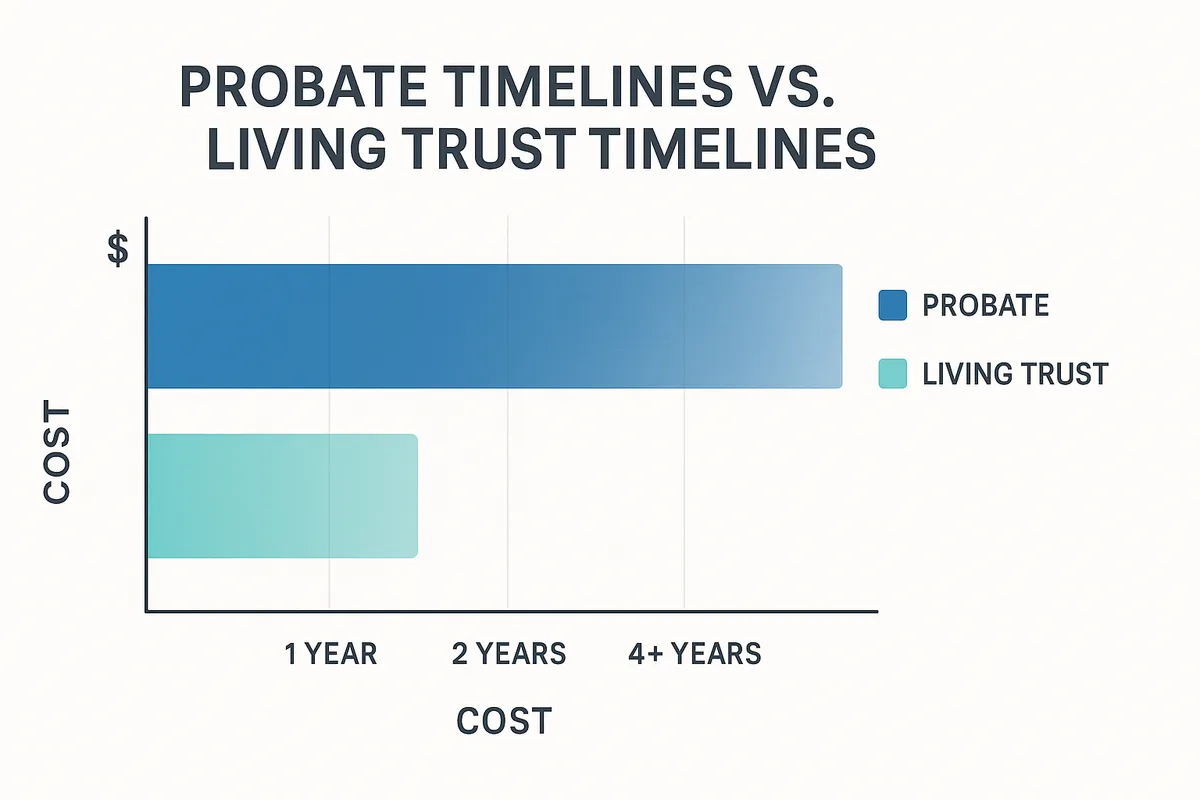

Example: Comparing Probate vs Living Trust Timeframes

Probate can take 6-12 months or longer, whereas a living trust can distribute assets within weeks.

- Beneficiaries receive timely support.

- Avoids prolonged uncertainty.

- Facilitates smoother transitions.

FAQ: Living Trust Questions Answered

1. What is a living trust?

A living trust is a legal document that holds and manages your assets during your lifetime and specifies how they are distributed after your death.

2. How does a living trust avoid probate?

Assets transferred into a living trust bypass the probate court, allowing faster and private distribution to beneficiaries.

3. Can I change my living trust after creating it?

If it is a revocable living trust, you can modify or revoke it anytime while you are alive and competent.

4. What assets should be included in my living trust?

Common assets include real estate, bank accounts, investments, and valuable personal property.

5. Who should be the trustee of my living trust?

You can be the initial trustee, but choose a reliable successor trustee to manage the trust if you become incapacitated or pass away.

6. Is a living trust the same as a will?

No, a living trust manages assets during life and after death without probate, while a will only takes effect after death and requires probate.

7. Do I need an attorney to create a living trust?

While you can use online tools, consulting an estate planning attorney ensures your trust complies with laws and suits your needs.

8. How much does it cost to set up a living trust?

Costs vary widely from a few hundred dollars using online services to several thousand with attorney assistance.

9. Can a living trust protect my assets from creditors?

Some trusts offer creditor protection, but revocable trusts generally do not. Consult a professional for asset protection strategies.

10. What happens if I don't fund my living trust?

Assets not transferred to the trust may have to go through probate despite having a trust.

11. Can a living trust help if I become disabled?

Yes, the successor trustee can manage your assets without court intervention if you become incapacitated.

12. Is a living trust private?

Yes, unlike wills, living trusts do not become public record when you die.

13. Can I include special instructions in my living trust?

Absolutely, you can set conditions for distributions, care of minors, or charitable gifts.

14. How often should I update my living trust?

Review it every few years or after major life events like marriage, divorce, or birth.

15. What is a pour-over will?

A will that transfers any remaining assets into your living trust upon death.

16. Can I serve as trustee and beneficiary?

Yes, in a revocable living trust, you often serve as both.

17. Are living trusts recognized in all states?

Yes, though laws vary, all U.S. states recognize living trusts.

18. Does a living trust avoid estate taxes?

Not necessarily; estate tax depends on federal and state laws and the size of your estate.

19. Can I create a living trust for my business?

Yes, business interests can be included in a living trust for smooth succession.

20. What if I move to another state?

You may need to update your trust to comply with new state laws.

21. Can a living trust expedite access to funds for emergencies?

Yes, the successor trustee can access trust assets quickly if you are incapacitated.

22. How does a living trust impact Medicaid eligibility?

Revocable living trusts do not protect assets from Medicaid spend-down rules.

23. Can I add assets to my living trust later?

Yes, you can transfer additional assets into the trust anytime.

24. What happens if my trustee dies or resigns?

The successor trustee named in the trust will step in to manage the trust.

25. Can I dissolve my living trust?

If revocable, you can dissolve it during your lifetime.

26. Are there different rules for irrevocable trusts?

Yes, irrevocable trusts cannot be changed once established and offer stronger asset protection.

27. How do I fund a living trust?

By retitling assets such as property and accounts in the name of the trust.

28. Can my living trust include digital assets?

Yes, you can specify management of digital accounts and online property.

29. What if I forget to fund my trust?

Assets not included will pass through probate; a pour-over will can help but may not avoid probate completely.

30. Does a living trust protect against family disputes?

Clear instructions in a trust can reduce conflicts but may not eliminate all disputes.

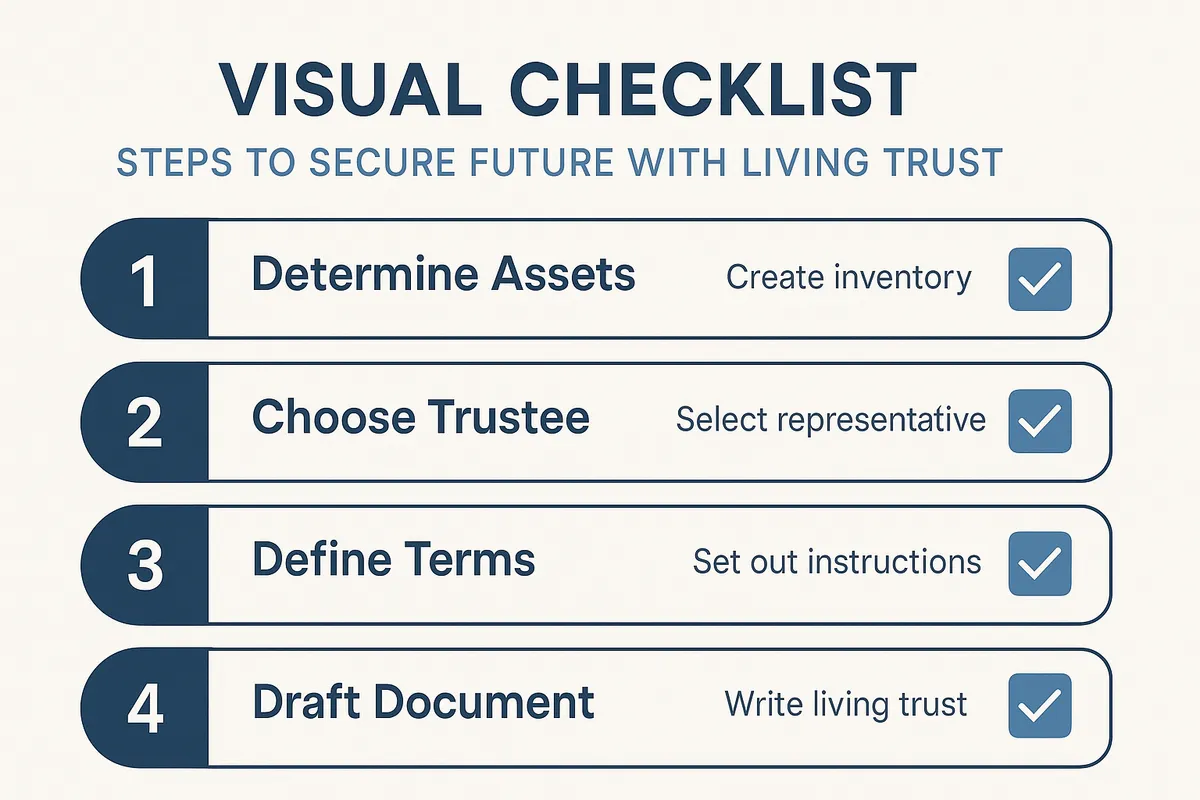

How to Set Up a Living Trust: A Step-by-Step Guide

Establishing a living trust may seem complex, but breaking it down makes the process manageable.

Step 1: Assess Your Assets and Goals

Start by listing your assets and clarifying your objectives.

- Include real estate, bank accounts, investments.

- Define who you want to benefit.

- Consider special instructions or conditions.

Step 2: Choose the Type of Trust

Select between revocable or irrevocable trust based on your needs.

- Revocable trusts allow changes.

- Irrevocable trusts offer stronger asset protection.

Step 3: Select a Trustee

Decide who will manage the trust.

- You can serve as initial trustee.

- Choose a reliable successor trustee.

- Consider professional trustees if needed.

Step 4: Draft the Trust Document

Work with an attorney or use reputable online services.

- Ensure legal compliance.

- Customize terms according to your wishes.

- Include provisions for incapacity.

Step 5: Fund the Trust

Transfer ownership of assets into the trust.

- Change titles on property and accounts.

- Update beneficiary designations if necessary.

- Maintain records of transfers.

Step 6: Keep Your Trust Updated

Review and revise your trust periodically.

- Reflect life changes like marriage or children.

- Adjust for new assets or laws.

- Keep your successor trustee informed.

Common Misconceptions about Living Trusts Debunked

Misunderstandings can prevent young professionals from utilizing living trusts effectively.

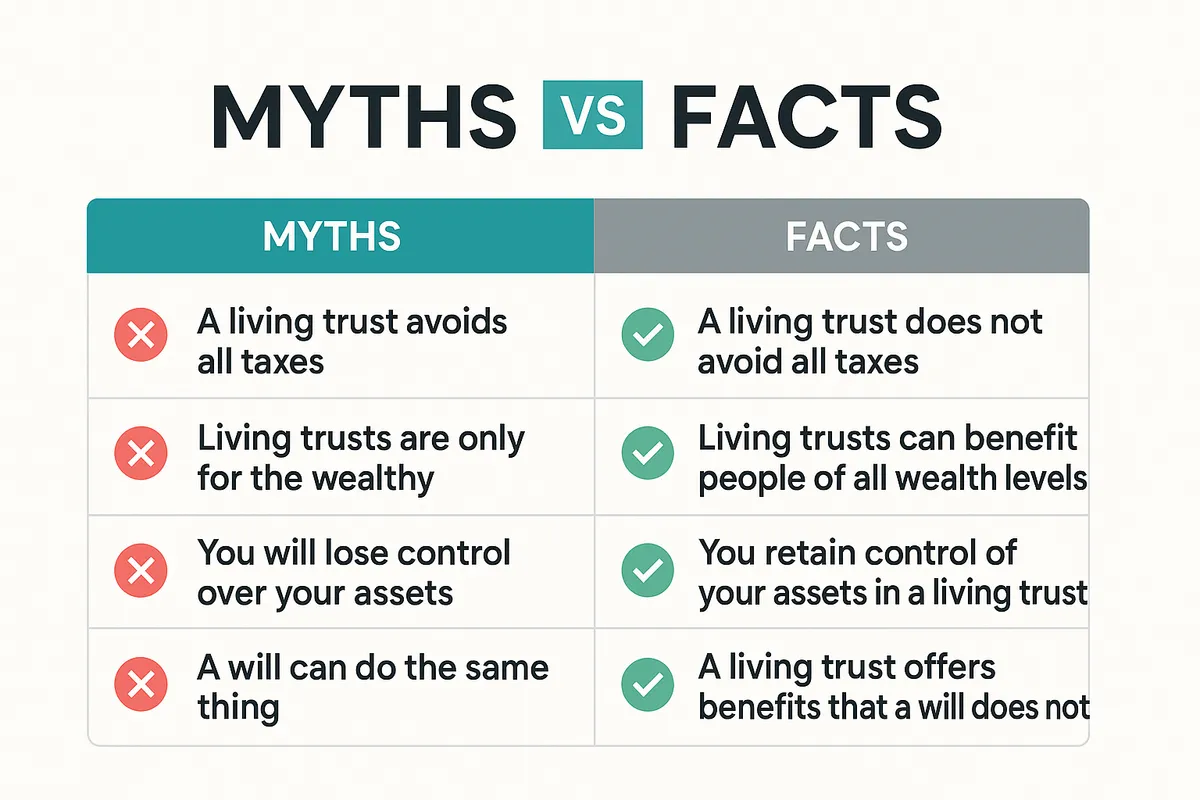

Myth 1: Living Trusts Are Only for the Wealthy

Reality: Anyone with assets can benefit.

- Protects modest estates.

- Simplifies transfers regardless of size.

- Provides control and privacy for all.

Myth 2: Living Trusts Avoid All Taxes

Reality: A living trust does not eliminate estate or income taxes.

- Tax obligations depend on current laws.

- Trusts can be structured for tax efficiency.

- Consult a tax professional for guidance.

Myth 3: Setting Up a Living Trust Is Too Expensive

Reality: Costs vary but can be affordable.

- Online tools reduce expenses.

- Professional advice ensures accuracy.

- Savings from avoiding probate often offset costs.

Myth 4: A Will Is Enough for Estate Planning

Reality: Wills go through probate, which trusts avoid.

- Trusts provide faster asset transfer.

- Offer more privacy and flexibility.

- Work well alongside wills for comprehensive planning.

Myth 5: Living Trusts Are Too Complicated to Manage

Reality: Once set up, trusts require minimal maintenance.

- Easy to update.

- Trustee manages assets smoothly.

- Clear instructions simplify administration.

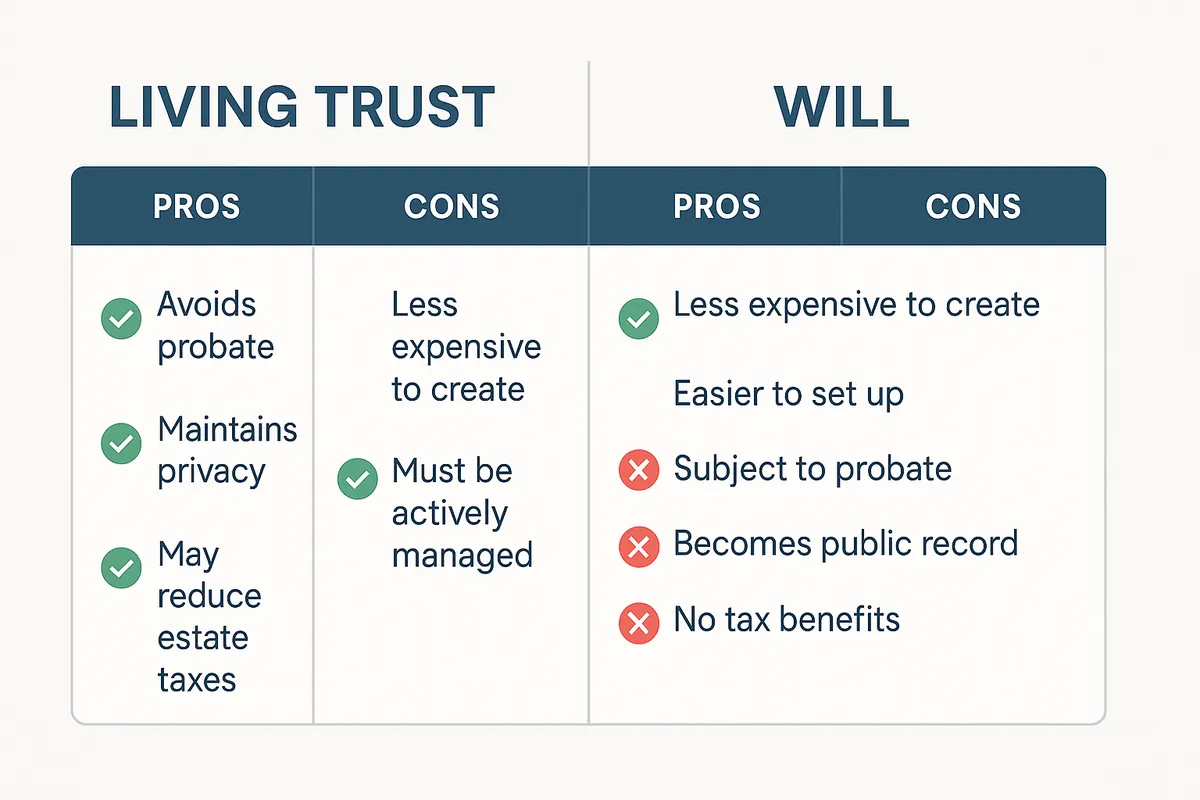

Living Trust vs. Will: Understanding the Differences

Both tools are essential but serve different purposes.

What a Will Covers

A will directs asset distribution and appoints guardians.

- Takes effect after death.

- Requires probate.

- Publicly accessible.

What a Living Trust Covers

Trust holds assets and manages them during life and after death.

- Avoids probate.

- Provides privacy.

- Allows incapacity planning.

When to Use Each

- Use a will to name guardians for minors.

- Use a living trust to manage significant assets.

- Often best to have both for full coverage.

Combining Living Trust and Will

A pour-over will transfers assets not included in the trust upon death.

- Ensures all assets are covered.

- Simplifies estate administration.

- Provides a safety net.

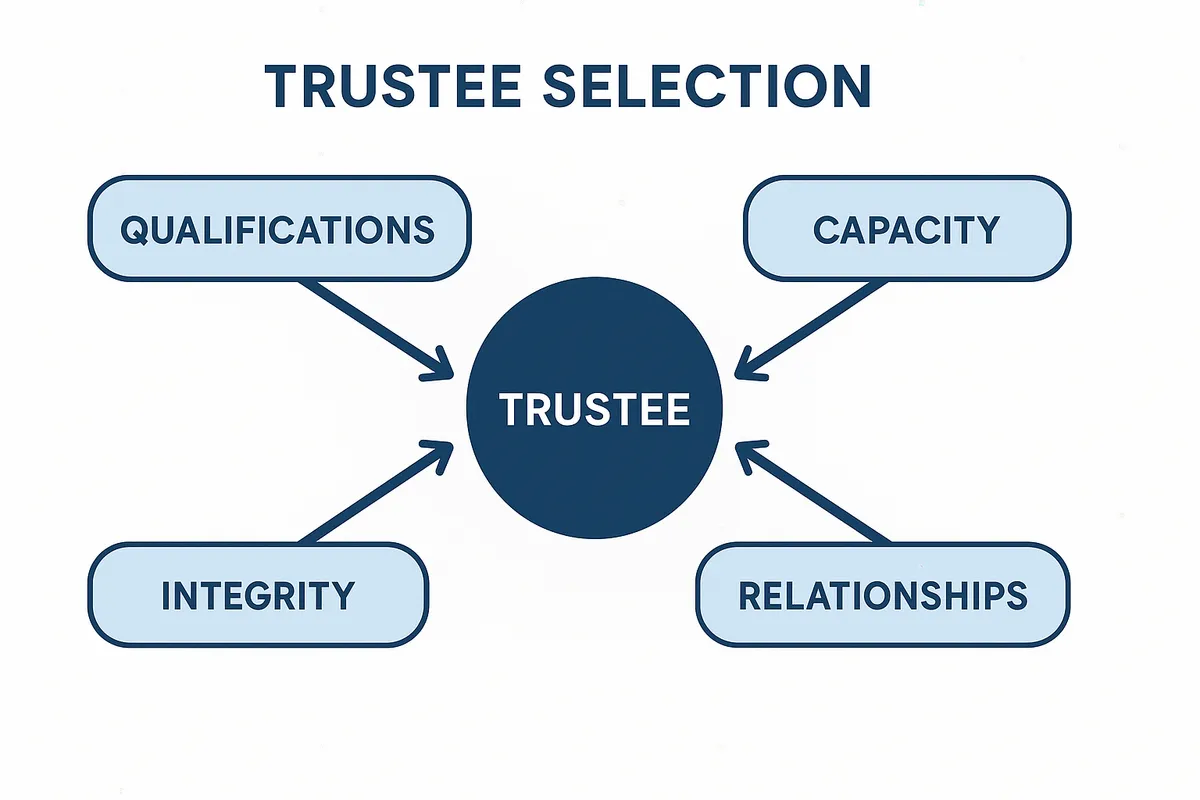

Choosing the Right Trustee: Tips and Considerations

Selecting the right trustee is critical to the success of your living trust.

Qualities to Look For

- Trustworthiness and integrity.

- Financial savvy and organization.

- Ability to act impartially.

Options for Trustees

- Yourself (initial trustee).

- Family members or close friends.

- Professional fiduciaries or trust companies.

Pros and Cons of Each Option

- Family may understand your wishes but could face conflicts.

- Professionals offer expertise but charge fees.

- Hybrid approach possible with co-trustees.

Communicating Your Expectations

- Clearly explain duties and responsibilities.

- Provide access to legal and financial advisors.

- Keep lines of communication open.

Preparing for Contingencies

- Name successor trustees.

- Outline procedures for trustee resignation or incapacity.

- Regularly review trustee arrangements.

Conclusion: Securing Your Future with a Living Trust

For young professionals, a living trust offers an effective way to protect your growing assets, avoid probate, and provide clear instructions for your estate. It ensures your family's security and peace of mind no matter what happens.

Taking the time to set up a living trust now can save your loved ones time, money, and stress in the future. Whether you're just starting your financial journey or have accumulated significant assets, this estate planning tool is a smart, flexible, and proactive choice.

Start planning today to secure your future and provide for what matters most.

Ready to take the next step? Consult an estate planning attorney or trusted advisor to create your personalized living trust.

Take the Next Step

If you own real estate or significant assets in California, creating a living trust is one of the most powerful ways to protect your family, avoid probate, and ensure your wishes are carried out. The Law Office of James Burns has guided thousands of families through the estate planning process, delivering clarity, confidence, and peace of mind. Call us today to schedule a confidential consultation.

📞 (949) 305-8642

🌐 www.jamesburnslaw.com

Disclaimer

This blog is provided for educational purposes only and does not constitute legal advice. Estate planning laws vary by state and change over time. Reading this blog does not create an attorney–client relationship. You should consult with a qualified estate planning attorney before making any decisions regarding trusts, wills, or related legal matters.

Intellectual Property Notice

© 2025 Law Office of James Burns. All rights reserved. FortressWall™ and Legacy Trust™ are proprietary frameworks of the Law Office of James Burns. This material may not be reproduced, distributed, or transmitted in any form without prior written permission, except for brief quotations used for non-commercial purposes with proper attribution.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment